The reality of 3% inflation

Everything costs more. In late 2026, inflation is sitting at 3.1%, a jump from the 2% average we used to rely on. You see it at the pump and the checkout counter every week. It isn't just in your head; your paycheck is objectively losing its buying power.

The reasons behind this are complex. We’re still feeling the ripple effects of supply chain disruptions from the past few years, coupled with increased demand as the economy recovers. Geopolitical events also play a role, impacting the cost of energy and essential goods. But understanding why doesn't necessarily make it easier to manage.

What does this look like in practice? A gallon of gas might be $4.50 where it was $3.50 last year. A weekly grocery bill that was $150 could easily be $175 or more. Even seemingly small increases add up quickly. Experts predict inflation will continue to moderate in the coming year, but significant price drops aren't likely. We need to adapt and find ways to protect our budgets.

Track every penny

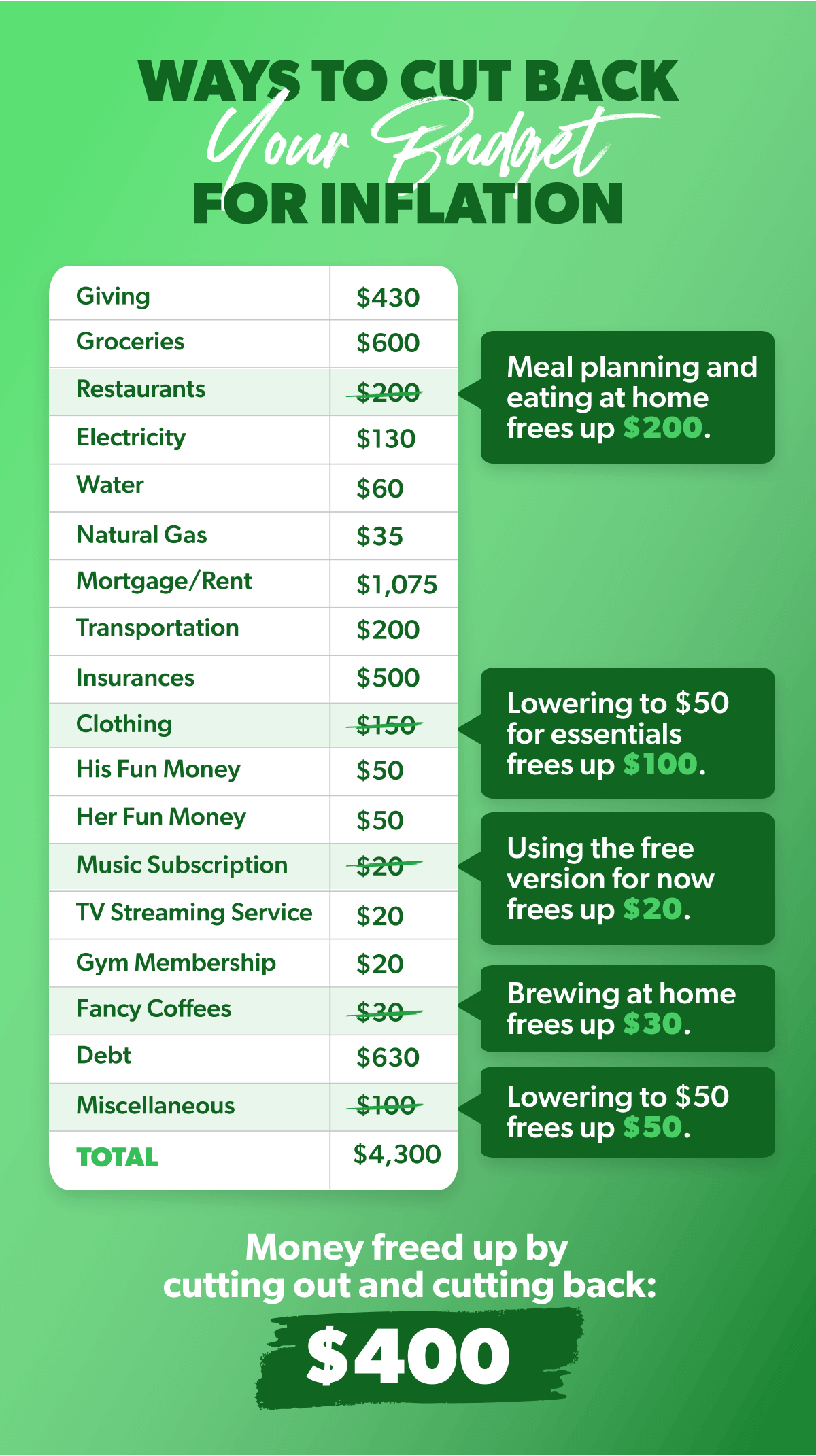

Before we get into specific strategies, let’s talk budgeting. It sounds restrictive, but I believe a good budget is actually liberating. It gives you control over your finances and allows you to prioritize what’s important. Resources like consumer.gov and consumerfinance.gov are excellent starting points for understanding the fundamentals.

A popular method is the 50/30/20 rule. This allocates 50% of your income to needs (housing, food, transportation), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment. It's a simple framework, but it requires honest self-assessment.

There are different approaches to how you budget. Zero-based budgeting requires you to allocate every dollar of your income to a category. The envelope system involves physically dividing cash into envelopes for different expenses. Budgeting apps like Mint and YNAB offer digital tools for tracking spending and setting goals. I'm not convinced one method is universally superior – the best approach is the one you’ll actually stick with.

15 Inflation-Busting Strategies for 2026

Okay, let's get down to brass tacks. Here are 15 actionable strategies to help you navigate this inflationary period.

1. Meal planning & cooking at home: Eating out is a major budget buster. Planning meals and cooking at home is almost always cheaper, and healthier. 2. Cut subscription services: Review your subscriptions. Are you really using all of them? Streaming services, gym memberships, and unused software can quickly drain your account. 3. Negotiate bills: Don't be afraid to call your internet, insurance, and cell phone providers and ask for a better rate. Often, they’ll be willing to negotiate to keep you as a customer.

4. Use cashback apps and browser extensions: Apps like Rakuten and Honey automatically find coupons and cashback offers when you shop online. 5. Shop at discount stores: Stores like Aldi and Dollar General offer significant savings on everyday essentials. 6. Buy in bulk (when it makes sense): Bulk buying can save money on non-perishable items, but be careful not to overbuy and waste food. 7. Energy conservation: Simple measures like turning off lights and unplugging electronics can lower your energy bill.

8. Repair instead of replacing: Before rushing to replace a broken appliance or item of clothing, see if it can be repaired. 9. Utilize library resources: Libraries offer free access to books, movies, music, and even online courses. 10. Find free entertainment: Take advantage of free community events, parks, and hiking trails. 11. Comparison shopping: Don’t settle for the first price you see. Compare prices at different stores before making a purchase. 12. Delay non-essential purchases: Do you need that new gadget right now, or can it wait? Delaying non-essential purchases can free up cash for more important expenses.

13. Side hustles: Consider taking on a side hustle to supplement your income. 14. Review insurance policies: Shop around for better rates on your auto, home, and life insurance. 15. Utilize store loyalty programs: Many stores offer rewards and discounts to loyalty program members. These small savings really add up over time.

Beating grocery store 'shrinkflation'

Grocery prices are a major pain point right now. It's not just that prices are higher, but we’re also seeing 'shrinkflation' – products getting smaller while the price stays the same. It’s frustrating, but there are ways to fight back.

Start by checking the unit price (price per ounce, pound, etc.) to compare different brands and sizes. Use coupons, both digital and paper. Plan your meals around what’s on sale each week. Apps like Flipp aggregate weekly ads from local stores, making it easy to find the best deals.

Reducing food waste is also crucial. Properly store leftovers, use up ingredients before they expire, and consider freezing food for later use. Don’t underestimate the savings from switching to store brands – they’re often just as good as name brands but significantly cheaper. Even small changes in your grocery shopping habits can make a big difference.

Name Brand vs. Store Brand Grocery Savings

| Category | Name Brand Average Price (per unit) | Store Brand Average Price (per unit) | Quality Difference | Overall Value |

|---|---|---|---|---|

| Cereal | $4.50 | $3.20 | Low | Good |

| Canned Vegetables | $1.20 | $0.85 | Medium | Excellent |

| Cleaning Spray | $4.00 | $2.75 | Medium | Good |

| Pasta (1lb box) | $1.80 | $1.30 | Low | Excellent |

| Over-the-Counter Pain Reliever (20 count) | $8.00 | $5.50 | Low | Good |

| Frozen Vegetables | $2.50 | $1.90 | Low | Good |

| Dairy Milk (gallon) | $3.99 | $3.29 | Low | Good |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

Energy Efficiency: Lower Bills, Bigger Savings

Utility bills are another area where inflation is hitting hard. Fortunately, there are several simple steps you can take to reduce your energy consumption and lower your bills. Switching to LED bulbs is a no-brainer – they use significantly less energy than traditional incandescent bulbs.

Unplug electronics when you’re not using them, as they continue to draw power even when turned off. Adjust your thermostat settings – lowering the temperature in the winter and raising it in the summer can save you money. Seal drafts around windows and doors to prevent heat loss.

Consider investing in energy-efficient appliances when it’s time to replace old ones. While the upfront cost may be higher, the long-term energy savings can be substantial. Many local utility companies offer rebates and incentives for energy-efficient upgrades, so be sure to check what’s available in your area.

What is your biggest budgeting challenge right now?

Vote below!

No comments yet. Be the first to share your thoughts!