Inflation is still here

Inflation isn't over. While the spikes of 2022 have calmed, prices are still high. The Bureau of Labor Statistics reported a 3.1% rise in the Consumer Price Index for the year ending January 2024. Everyday life costs more than it did three years ago, and most forecasts suggest we'll see another 2.5% to 3% increase through 2026.

Many forecasts suggest inflation will settle around 2.5% to 3% in 2026. This isn’t cause for panic, but it is a signal that we need to adapt our financial strategies. This isn't about hoping for prices to fall back to 'normal'; it's about building a budget that can withstand ongoing price pressures. We’ll focus on practical, actionable steps you can take now to stretch your dollar further.

Budgeting isn't about suffering; it's about making sure your money goes where you actually want it to go. You can maintain your lifestyle if you're intentional about where the leaks are.

Zero-based budgeting

Anthony, a contributor at BuzzFeed, uses zero-based budgeting to manage his money. The idea is to give every dollar a job before the month starts. You decide where the money goes ahead of time so you aren't left wondering why your bank account is empty on the 25th.

Let's look at an example. Imagine you bring home $2000 per month. Using zero-based budgeting, you wouldn't just pay your bills and spend the rest. Instead, you’d allocate every dollar. Perhaps $800 for rent/mortgage, $300 for groceries, $200 for transportation, $100 for utilities, $100 for debt repayment, $200 for savings, and $300 for wants (entertainment, dining out, etc.).

The key is that your income minus your expenses always equals zero. If you have money left over, don’t just let it sit there. Assign it to a savings goal, debt payoff, or a "fun money’ category. This method requires discipline, but it’s incredibly effective for understanding your spending habits and prioritizing what truly matters. It"s about aligning your spending with your values.

Digital envelopes

The envelope system is a classic budgeting technique that’s seen a resurgence in popularity, especially with the help of apps like Goodbudget. Traditionally, you’d physically divide your cash into envelopes labeled for different spending categories – groceries, gas, entertainment, etc. Once an envelope is empty, you're done spending in that category for the month.

Goodbudget brings this concept into the digital age. You create 'envelopes' within the app and allocate a specific amount of money to each one. As you spend, you track your transactions against those envelopes. The visual representation of your envelope balances dwindling can be surprisingly motivating.

The power of the envelope system, whether physical or digital, lies in its simplicity and the immediate feedback it provides. It forces you to be mindful of your spending and prevents overspending in any one area. It's not just about tracking where your money goes, it's about feeling the impact of each purchase.

Small wins

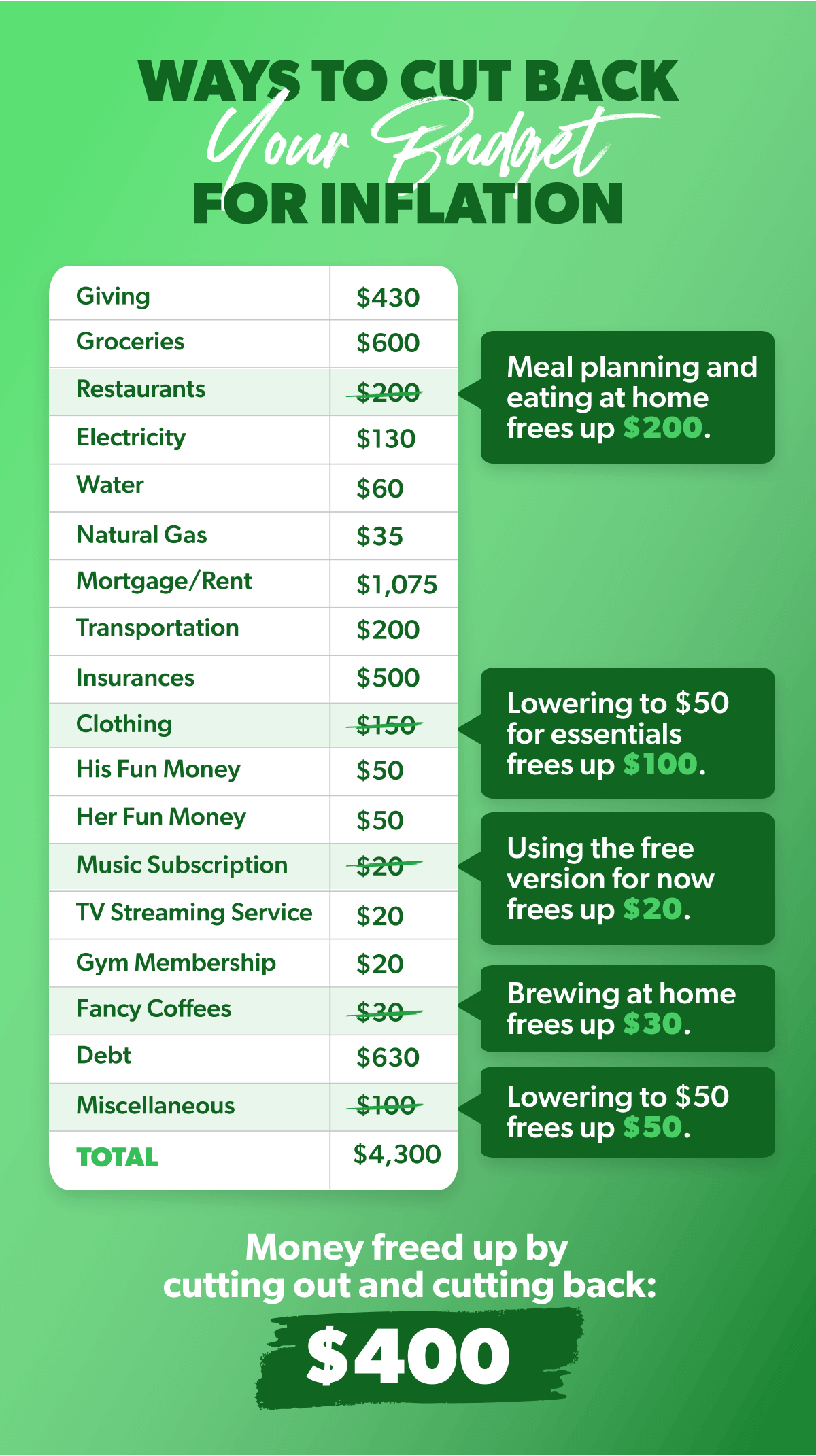

Often, the biggest impact on your budget comes from a series of small changes. These 'micro-budgeting' tactics might seem insignificant on their own, but they add up quickly. Brewing coffee at home instead of buying it daily, packing your lunch instead of eating out, and canceling unused subscriptions are all great starting points.

A recent video from FOX 11 Los Angeles highlighted several effective strategies. They suggest reviewing your insurance policies annually to shop for better rates, utilizing free library resources instead of purchasing books and movies, and taking advantage of free entertainment options in your community. These are all low-effort ways to save money.

Don't underestimate the power of cutting back on convenience costs. A $5 daily coffee run adds up to over $150 per month. Small, consistent choices like these can free up a significant amount of money for your savings goals. It’s about finding areas where you can make adjustments without drastically altering your lifestyle.

- Brew coffee at home.

- Pack your lunch.

- Cancel unused subscriptions.

- Use library resources.

- Review insurance policies annually.

Negotiate your bills

Many people are hesitant to negotiate bills, but it’s a surprisingly effective money-saving strategy. Call your internet provider, phone company, and insurance provider and ask if they can offer you a better rate. Often, they will, especially if you mention competitor pricing.

Before you call, do your research. Find out what other companies are charging for similar services. Having this information will strengthen your negotiating position. Websites like NerdWallet and Bankrate can help you compare prices.

It’s okay to be polite but firm. A simple script could be: “I’ve been a loyal customer for [number] years, and I’m currently paying [amount]. I’ve seen competitor offers for [amount]. Can you match that or offer me a lower rate?” Don't be afraid to walk away if they can’t meet your needs.

Meal planning for real life

Meal planning is often touted as a budgeting essential, but it’s about more than just finding recipes. The real savings come from inventorying your pantry and refrigerator before you plan your meals. What do you already have on hand that you can use? Building meals around existing ingredients minimizes food waste and reduces your grocery bill.

Focus on creating meals that utilize similar ingredients to avoid buying unnecessary items. For example, if you buy a head of broccoli, plan multiple meals that incorporate it. This also reduces the chances of food spoiling before you can use it.

Planning your meals around sales and seasonal produce is another key strategy. Check your local grocery store's weekly ads and plan your meals accordingly. Batch cooking – preparing large quantities of food at once – can save you time and money throughout the week. It also helps resist the temptation to order takeout.

Budgeting tools

There’s a wealth of budgeting apps and tools available, each with its own strengths and weaknesses. Goodbudget, as we’ve discussed, excels at the envelope system. Mint is a popular free option that aggregates all your financial accounts in one place.

YNAB (You Need a Budget) is a more comprehensive, but also more expensive, option that focuses on proactive budgeting and giving every dollar a job. Other options include Personal Capital (focused on investment tracking) and PocketGuard (focused on spending limits).

The 'best' tool depends on your individual needs and preferences. If you’re new to budgeting, a free app like Mint might be a good starting point. If you’re looking for a more robust system, YNAB or Goodbudget could be a better fit. Experiment with a few different options to find what works best for you.

Budgeting App Features Comparison

| App Name | Ease of Use | Customization | Reporting | Cost |

|---|---|---|---|---|

| Goodbudget | Generally Easy | Highly Customizable | Detailed Reports | Offers Free and Plus versions |

| Mint | Easy to Navigate | Moderate Customization | Basic Reports | Free |

| YNAB | Moderate Learning Curve | Extremely Customizable | Robust Reporting | Subscription Based |

Illustrative comparison based on the article research brief. Verify current pricing, limits, and product details in the official docs before relying on it.

No comments yet. Be the first to share your thoughts!